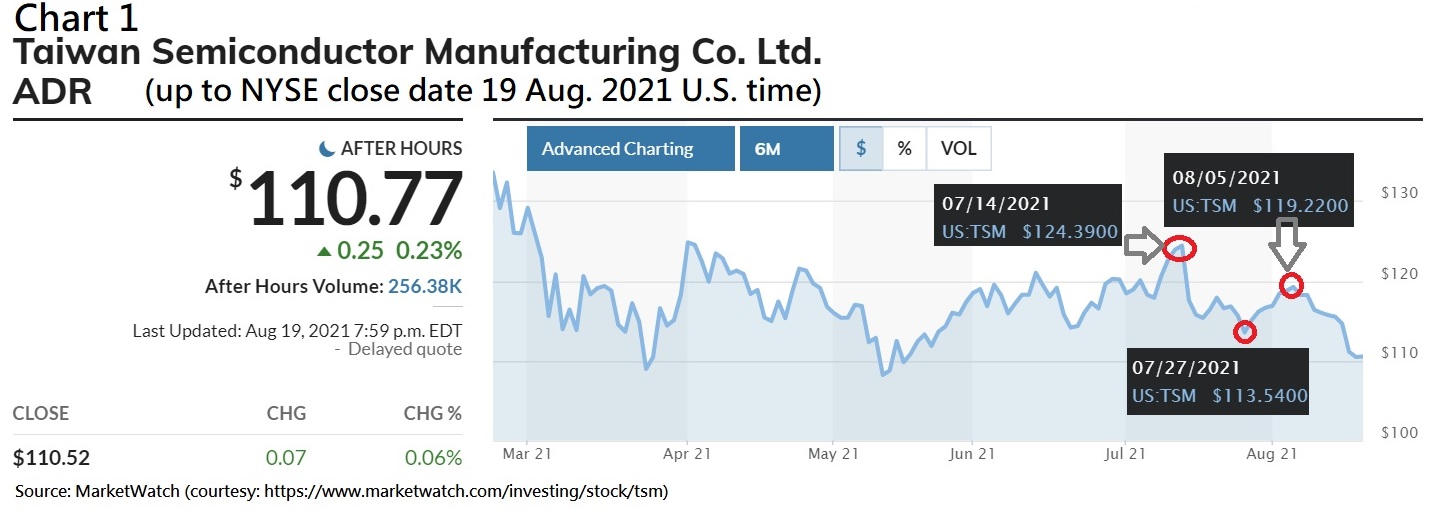

The Semiconductor sector in China regularly attracts attention from the global investment community. The recent regulatory crackdown by China’s tightening policy has panicked investors and turned investors attention to regional semiconductor stocks. Being a regional flagship stock, Taiwan’s Taiwan Semiconductor Manufacturing Co., Ltd (TSMC) has taken advantage of China’s regulatory storm and now outranks regional tech giant Tencent as the most valuable stock in Asia. The regulatory crackdown from July to August has eroded the market capitalization of Tencent and its tech peers except TSMC which is now worth over USD $540 billion. The period from July to August still sees TSMC’s ADR price climbing up and reaching recent price peaks of USD $124.39 & USD $119.22

amidst recent tenure of tech stock’s price slumping. China’s Guotai CES Semiconductor Industry ETF which tracks semiconductor stocks in China has seen the price peak at RMB1.76 in July, reflecting optimistic sentiment over the semiconductor industry in China.

Apart from being a shelter from China’s regulatory storm, the regional semiconductor sector presents strong fundamentals attracting investors’ attention. These factors include surging end-users in the markets of smartphones and automobiles, enormous regional investment in the electrical and electronic fields, hike in regional consumption of semiconductor components as well as increasingly important role of the Asian semiconductor supply chain in the global market. This macro-environment strengthens investor confidence in the semiconductor sector within the region.

Major players in the region

In Asia the “Big 4” semiconductor players are China, Japan, South Korea and Taiwan. They present different core competencies across the global semiconductor value chain (Chart 3). Their emergence as dominant players in this sector are a testamnet that companies worldwide rely heavily on Asian semiconductor manufacturers more than ever.

China

China’s enormous population helped shift China’s semiconductor consumption pattern and presents giant internal demand. According to Deloitte, 75% of China’s home-made semiconductor products will be consumed internally by 2035 and local spending in semiconductor equipment will become the largest household expense in next 5 years. Growth of migrant workers, concentration of key suppliers and skill upgrading help enlarge the Chinese semiconductor market. National policies strengthening 5G infrastructure construction and enabling 5G smartphones production capacity further drive semiconductor consumption. China’s semiconductor stock will continue to enjoy strong domestic demand for their products. Top revenue-earners include H.K.-listed SMIC which is the largest semiconductor foundry in China.

Japan

Compared with the other Big 4, Japanese players depict less strength across the semiconductor value chain

but substantial advantages in the upstream supply chain of materials. Japan’s core competences are in raw materials, equipment and small active-passive components. For example, Japan is the largest supplier of raw materials for photoresist manufacturing which supports South Korea’s DRAM’s (Dynamic Random Access Memory) supply chain. Any interruption to Japan’s supply would decrease South Korea’s output value by over USD $60 billion and erode electronics foundry industry’s global revenue by over USD $700 billion. Top revenue-earning semiconductor players from Japan include Sony, Kioxia, Renesas and ROHM. However, Japanese stocks face downward price pressure due to strong regional competition from South Korea which challenges Japan’s dominant sourcing position of semiconductor raw materials.

but substantial advantages in the upstream supply chain of materials. Japan’s core competences are in raw materials, equipment and small active-passive components. For example, Japan is the largest supplier of raw materials for photoresist manufacturing which supports South Korea’s DRAM’s (Dynamic Random Access Memory) supply chain. Any interruption to Japan’s supply would decrease South Korea’s output value by over USD $60 billion and erode electronics foundry industry’s global revenue by over USD $700 billion. Top revenue-earning semiconductor players from Japan include Sony, Kioxia, Renesas and ROHM. However, Japanese stocks face downward price pressure due to strong regional competition from South Korea which challenges Japan’s dominant sourcing position of semiconductor raw materials.

South Korea

South Korea is the major supplier of memory chips, accounting for over 40% of global supply. Although China pursues self-sufficiency policy for its semi-conductor industry, China still relies on advanced below 10nm chips provided by South Korea. This means that South Korean players still control a solid market position with leading-edge logic foundry process technology. Top revenue-earning semiconductor players from South Korea include Samsung Electronics & SK Hynix. Samsung is Asia’s leading semiconductor company which works on in IC design, smart phones and wafer manufacturing. SK Hynix is the global leader in DRAM and NAND Flash market for many years. Semiconductor stocks in South Korea are poised for optimistic prospects by thier dominant position in global semiconductor industry.

Taiwan

Taiwan has a complete semiconductor industry chain, production clusters and R&D capabilities. According to Market-Prospects.com, Taiwan provides over 90% of the advanced logic IC production capacity (below 10nm) and 40% of logic IC products both in the world. This proves that Taiwanese players are extraordinarily competent and competitive in chip manufacturing and IC design thanks to their core competence of owning the world’s biggest foundry and most advanced semiconductor manufacturing process technology. Together with South Korean players, Taiwanese companies are also the major suppliers of advanced below 10nm chips for China. Top revenue-earning semiconductor players from Taiwan include TSMC & MediaTek of which TSMC dominates global semiconductor foundry market. Seeing Taiwan’s semiconductor industry continuing to grow, investors should be optimistic about the prospects of Taiwan’s semiconductor stock.

{kind=link}