As we bid farewell to 2023, the U.S. Federal Reserve has indicated an end to its aggressive interest rate hikes, and interest rate cuts are on the horizon. This significant shift ushered in a new era of economic policy, prompting investors globally, including those focused on key markets like Hong Kong, China, and all of Asia, to reassess their strategies for 2024. This turning point presents an opportunity for investors to reflect and plan strategically as they navigate the ever-changing economic landscape.

The Change of Interest Rate Cycle

Since March 2022, the Fed has hiked rates 11 times, totalling a 525 basis-point increase. This aggressive stance was pivotal in taming inflation, but now, a more dovish approach is anticipated as market dynamics evolve. Analysts widely predict at least three rate cuts in 2024, a forecast that has already energized equity markets.

Why is this change monumental? A resilient yet slowing economy and inflationary pressures that, while persistent, are showing signs of easing. The Fed Chair, Jerome Powell, hints at a cycle peak, making further hikes unlikely. While not explicitly confirming the end of the hiking cycle, this dovish turn sets a new stage for economic stimulus through rate reductions.

Market Implications

According to Ellen Zentner of Morgan Stanley, the initiation of a rate cut is expected in June 2024, followed by a gradual descent to 2.375% by 2025. This aligns with a strong dollar, indicating a favourable time for long-dollar positions.

On the other hand, Yan Zhaojun of Zhongtai International sees the end of the hiking cycle as a response to a moderate labour market slowdown and tightening financial conditions. His outlook suggests a more gradual easing, with a 50-75 basis-point cut throughout 2024.

UBS Wealth Management, however, cautions against overly aggressive rate cut expectations, advocating for a more measured approach aligned with the Fed’s guidance.

Strategic Shifts in a New Interest Rate Environment

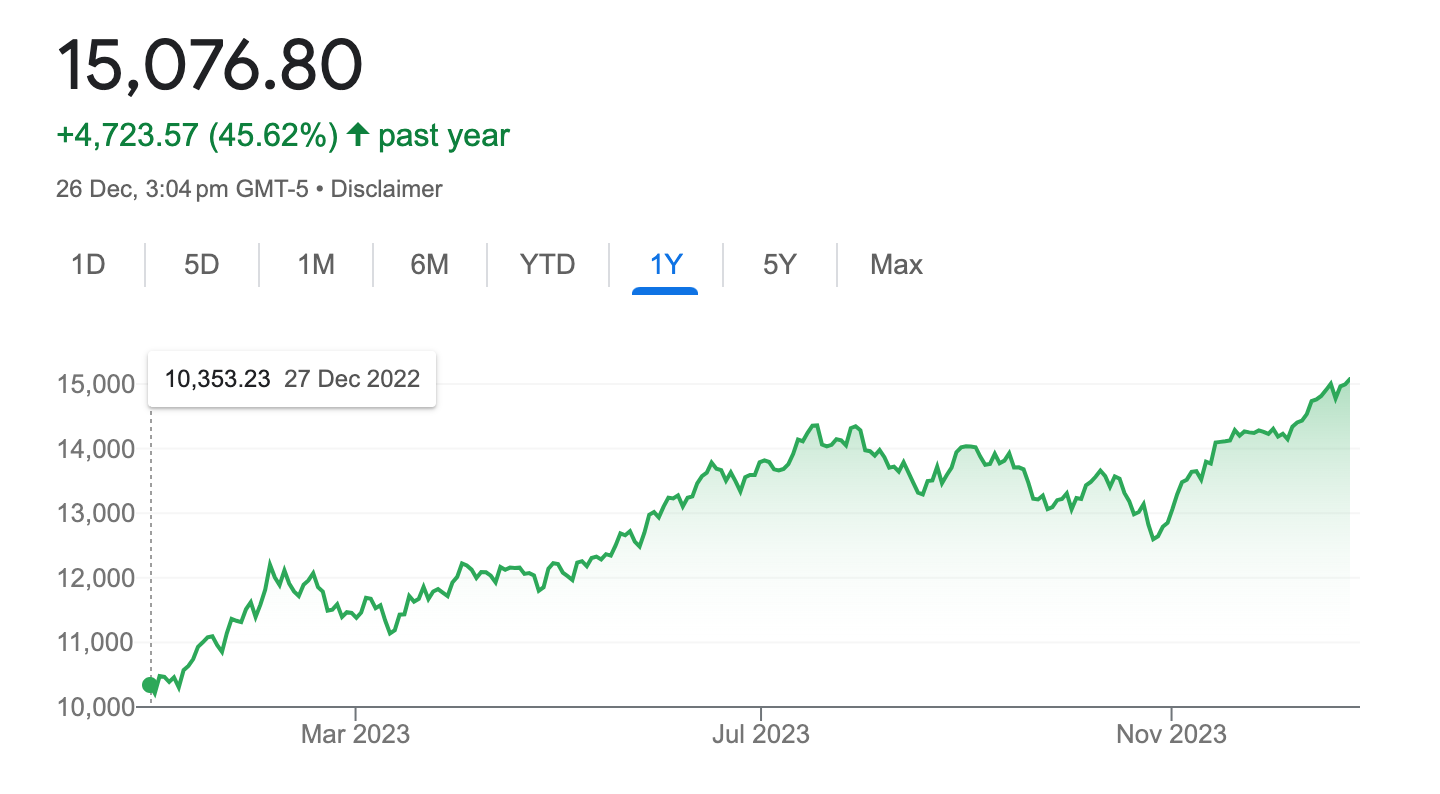

Asian investors are expected to continue investing in tech stocks, especially the U.S. giants, in 2024. The NASDAQ Composite Index is predicted to remain positive after it experienced an impressive surge of over 40% in 2023, thanks to a rare combination of favourable factors.

The Federal Reserve’s policy shift towards a more accommodating stance creates a favourable environment for growth in tech stocks. This policy change is a macroeconomic adjustment and a direct booster for the high-growth tech sector.

Tech companies have been focusing on cutting costs since the beginning of 2023. This focus on efficiency and profitability sets these companies up for a stronger financial footing, further enhancing their appeal to investors.

The surge in interest around Artificial Intelligence (A.I.) themes is fueling a new wave of investment. The fascination with A.I. is not limited to niche sectors; it’s spurring growth in various related stocks, from A.I. chips and software to essential infrastructure.

Beyond the tech sector, 2024 also focuses on emerging markets and commodities. In the commodities sector, gold shines as a hedge against uncertainty. As the world shifts towards renewable energy, copper’s unique position as both a financial and industrial asset could drive its price up.

Hong Kong and China Markets

As the U.S. Federal Reserve leans towards reducing interest rates, there is a consequential shift in the global financial landscape, particularly impacting the markets of Hong Kong and China. A decrease in U.S. rates typically leads to a weakened dollar, enhancing the attractiveness of emerging markets. This shift could significantly benefit businesses with foreign currency assets and liabilities in these regions. In such an environment, while global stock indices might show a general weakness due to a potential economic slowdown, emerging markets like China are expected to demonstrate relative resilience. This scenario will likely foster an influx of foreign investment into Chinese stocks, revitalizing the market with improved liquidity.

Hong Kong’s market is expected to benefit from the policy change positively. The recent rate cuts could result in a weaker U.S. dollar, leading to an RMB appreciation. This would ease the valuation and liquidity pressures on Hong Kong stocks. Additionally, the interest rate differential between Hong Kong and the U.S. will likely narrow, and China’s nominal GDP growth is expected to rebound. These factors could result in a resurgence of capital inflows in Hong Kong’s markets.

Navigating Uncertainties with Strategic Diversification

While the anticipated rate cuts offer new opportunities, investors must tread cautiously. The economic landscape of 2024 is complex, and the possibility of a less-than-smooth economic landing remains. The markets face headwinds if economic downturns are more pronounced than expected. In such a scenario, a strategy focused on diversification, targeting sectors poised for growth despite broader economic challenges, will be crucial.

{kind=link}