The recent strategic shift by the U.S. Federal Retirement Thrift Investment Board (FRTIB) to exclude Chinese and Hong Kong stocks from its I Fund’s investment portfolio signifies a pivotal moment for Hong Kong’s financial market. With a colossal asset size of $771 billion, the FRTIB’s decision not only redefines its investment trajectory but also could send ripples, particularly impacting Hong Kong’s stock market.

More Than Just A Strategic Shift in Investment

FRTIB’s move away from Chinese and Hong Kong markets is not just an isolated fiscal decision. With an asset size of $771 billion, the impact of this decision is far-reaching. The I Fund, previously tracking the MSCI Europe, Australasia, and Far East Index, will now follow the MSCI All Country World Ex-U.S. Index. This transition to a more globally diversified index excluding U.S., China, and Hong Kong markets underscores a strategic shift towards mitigating geopolitical risks and market volatilities.

But why this change? The Fund’s advisory firm Aon Plc points to a blend of factors: increasing uncertainties in Chinese and Hong Kong markets, U.S. restrictions on investments in sensitive Chinese industries, the delisting of Chinese companies from U.S. exchanges, and sanctions on Russian securities. These factors have heightened the trade costs and volatility of returns, prompting a re-evaluation of the risk-reward balance.

The FRTIB’s decision reflects a broader global trend where funds increasingly seek to diversify away from geopolitical risks. The suggestion within the U.S. to establish “Asia Ally” funds, focusing on markets friendly to the U.S., indicates a growing desire to decouple from the tensions associated with China-related investments.

The new benchmark index includes 5,621 stocks from 21 developed and 23 emerging markets, accounting for 90% of the stock market value outside the United States. In fact, this Fund has never invested in mainland China, and the proportion of Hong Kong stocks in this index is less than 4%, but still, we cannot overlook the significance of this withdrawal decision.

Can Mainland Chinese Capital Compensate for International Withdrawal in Hong Kong’s Market?

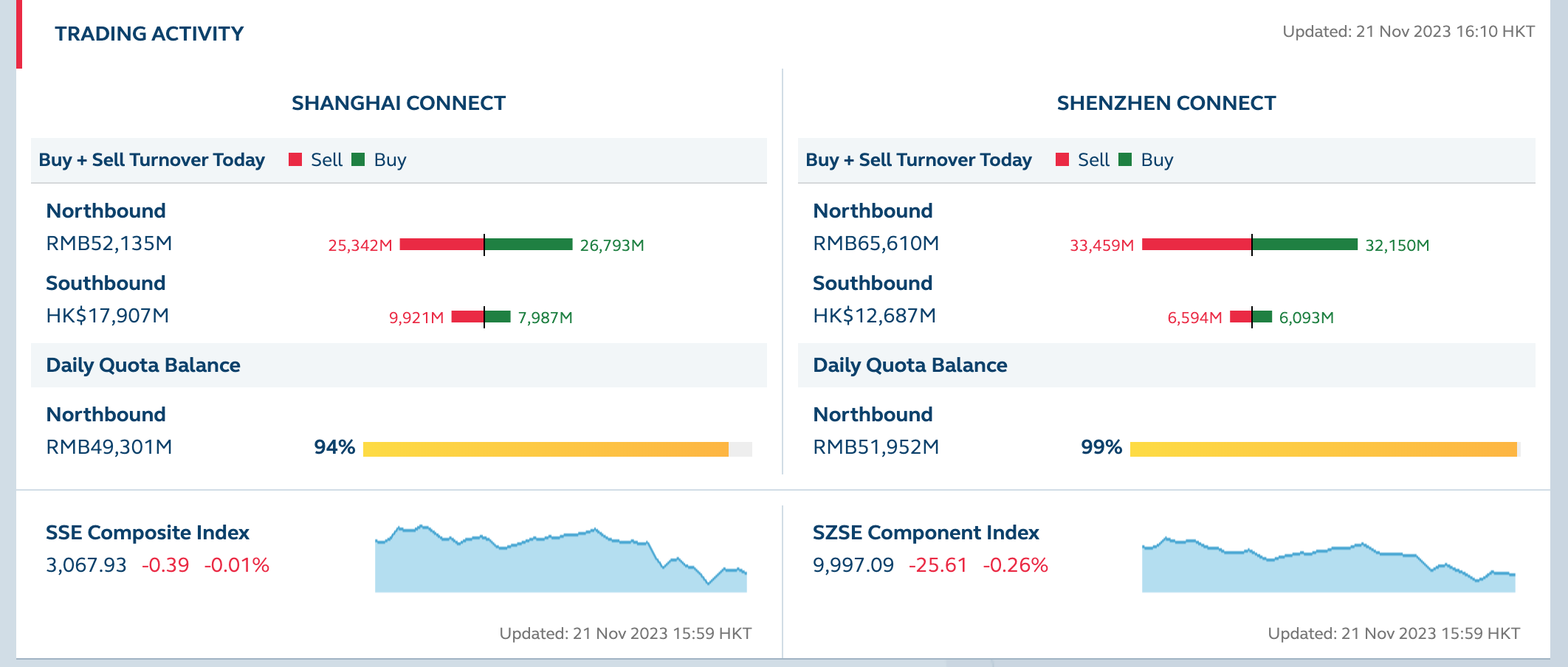

What does this mean for Hong Kong’s stock market? International funds have traditionally dominated Hong Kong as a renowned global financial hub. However, the recent developments have decreased its influence, with foreign institutional investors’ transaction volume dropping from 42% in 2011 to 36% in 2020.

Meanwhile, the increased influence of mainland Chinese capital in Hong Kong’s market, primarily through the Stock Connect programs, has altered the investment landscape. According to statistics from Huatong Securities, the net inflow of Chinese capital into the Hong Kong stock market exceeded 380 billion Hong Kong dollars in 2022. The transaction volume of this capital already accounts for about 25% of the average daily transaction volume of the Hong Kong stock market, becoming a significant force influencing the market.

Hong Kong’s stock market was once significantly buoyed by these foreign investment funds. With their substantial investment capital and long-term horizons, these funds provided a stabilizing force. The withdrawal of such funds could lead to increased market volatility and decreased upward momentum, as the Chinese capital inflows tend to be less substantial, more short-term, and more susceptible to policy changes.

Also, the predominance of Chinese investment could impact international perceptions of market maturity and openness. Therefore, while Chinese capital can provide significant support, a balanced and diversified investment portfolio remains crucial for the market’s long-term health and attractiveness.

The decision by the FRTIB represents a significant shift, not just in investment strategy but in the broader narrative of global finance. How Hong Kong’s market will adapt to these evolving dynamics remains a crucial question, as does the potential for other international funds to mimic the FRTIB’s reduction in exposure to Chinese and Hong Kong stocks. Its impact extends beyond immediate market reactions, potentially reshaping the contours of international investment flows.

{kind=link}